Being your own boss in trucking starts with one truck, and one big decision. Many drivers dream of becoming owner-operators because it means more freedom and, possibly, better pay. But it also means you’re in charge of everything: the costs, the risks, the choices.

This guide is built for two kinds of readers:

- New drivers thinking long-term.

- Company drivers ready to make the jump and buy their own truck.

I’ll walk through the basics:

- What types of loads you can haul.

- What it really costs to get started.

- How much you might make.

- The rules you’ll need to follow.

- And simple tips to help you run your truck like a business.

By the end, you’ll have a solid sense of what this road looks like — and whether it’s the right one for you.

Types of Hauls: Long-Haul, Regional, and Specialized Freight

As an owner-operator, you can choose the kind of work that fits your goals. Most hauls fall into three main categories: long-haul, regional, or specialized freight. Each option comes with different equipment, income levels, and time away from home.

Long-Haul (OTR) Trucking

OTR stands for over-the-road. These are long-distance runs, often from coast to coast. You’ll be out for weeks at a time, living in your truck. Most OTR drivers cover the entire country. Some also run into Canada or Mexico.

It’s common to log more than 100,000 miles per year in this role. That means more fuel, more wear on your truck, and more time on the road. But it also means more chances to earn.

OTR drivers typically run on highways and interstates. Since they’re not home every night, they need sleeper cabs.

Many new drivers start with OTR. It’s a good way to gain experience and rack up miles. Some stick with it for the freedom and the access to national freight.

Rates in OTR can vary. The national spot market affects your per-mile pay. Long-haul also brings higher fuel bills. Still, the total income can beat what you’d earn staying local.

Regional Trucking

Regional drivers stick to one area — like the Midwest or Southeast. The radius might be a few hundred to a thousand miles. They often get home more often. Some return weekly, others every few days.

Most regional hauls are single-stop loads. The distances are shorter than OTR but longer than local routes. You won’t be out for weeks, which makes it easier to balance work and home life.

Pay is usually lower than OTR, but so are the miles. Many regional drivers use sleeper trucks, but not always. This type of work is a common next step for drivers leaving OTR. It offers steady loads without being gone for too long.

Specialized Freight

This includes anything that needs extra care, special gear, or a permit. Think flatbeds, tankers, oversized equipment, hazmat, or livestock. These hauls usually pay better because fewer drivers are trained or equipped to take them.

If you want to move into this space, you’ll need the right gear and paperwork. That could mean getting a hazmat or tanker endorsement. It could mean buying tarps, chains, or even a specialized trailer. You’ll also need to follow added safety rules and routing limits.

The cost of getting started can be high. But the rates often make it worth it. For example, hauling wind turbine parts or chemical tankers pays well. Not everyone wants that kind of responsibility, which keeps the competition low.

Choosing What Fits

Every haul type affects your income, your equipment, and your time at home. You might run dry van freight across the country, refrigerated loads within five states, or fuel tankers in a tight niche. There’s no one right answer. Over time, most owner-operators find a lane that fits their lifestyle and income goals.

💡 An owner-operator could choose to haul general dry van freight coast-to-coast as an OTR driver, run regional refrigerated loads in a 5-state area, or focus on a specialized niche like tanker hazmat routes. Each path will influence the kind of truck and trailer you need, how often you’re home, and the freight rates you can charge. Many owner-operators eventually find a niche that suits their income goals and lifestyle, whether that’s chasing the highest-paying specialized loads or sticking to a predictable regional lane that gets them home regularly.

Financial Considerations: Startup Costs, Ongoing Expenses, and Income

Money is one of the biggest pieces of the puzzle when you’re going out on your own. You’re no longer just a driver. You’re running a business. That means you cover the big purchases, the recurring bills, and everything in between.

This section breaks it all down:

- What it costs to get started

- Whether to buy or lease a truck

- The monthly bills to expect

- How much you might actually earn

Startup Costs to Become an Owner-Operator

Starting out isn’t cheap. Some of the upfront items you’ll need to pay for include:

- Buying or leasing a truck

- Possibly buying a trailer

- Getting your CDL (if you don’t already have one)

- Business setup and registration fees

- Permits and authority setup (like FMCSA, IRP, UCR)

- First-year insurance premiums

Let’s talk trucks first.

A used truck might cost anywhere from $30,000 to $80,000 depending on age, mileage, and condition. A new truck could run well over $120,000. Some with high-end features even push past $180,000.

If you need a trailer too, plan for more. A dry van might cost $30,000 or more. Refrigerated trailers often start around $60,000.

To lower upfront costs, some drivers lease trailers or pull one provided by a carrier.

You’ll also need insurance. If you’re running under your own authority, expect to pay $15,000 or more per year for your first policy. This number can drop later if you maintain a clean record.

Keep in mind: If you lease on with a carrier, they may cover some costs like plates, permits, and even part of your insurance. If you go fully independent, all of it is on you.

Most of these startup costs are one-time or yearly. They’re your cost to enter the business. Once you’ve cleared this stage, the next challenge is keeping up with monthly expenses while turning a profit.

How to Decide Between Buying and Leasing a Truck?

One of the biggest choices you’ll make as an owner-operator is how to get your truck. You can either buy it or lease it. Both options have tradeoffs in cost, control, and long-term value.

Let’s break it down so you know what to expect.

Upfront Costs

Leasing usually costs less upfront. You might only need a few thousand dollars for the first payment or deposit. That makes it easier to get started if cash is tight.

Buying a truck takes more. Most lenders expect a down payment of 10 to 20 percent. On a $100,000 truck, that’s $10,000 to $20,000 before you even get behind the wheel.

Monthly Payments

Lease payments are often lower than loan payments for the same truck. But those payments don’t end unless you stop leasing. That means you’ll always have a monthly expense if you stick with leases.

If you buy and finance your truck, the payments might be higher each month. But once the loan is paid off, the truck is yours. No more payments. That’s a major advantage if you plan to stay in the business long-term.

Total Cost Over Time

Buying usually costs less in the long run. With every loan payment, you build ownership. When the truck is paid off, you still have an asset — something you can keep using, trade, or sell.

Leasing doesn’t give you that. Unless you’re in a lease-to-own program, the truck isn’t yours. After years of payments, you could walk away with nothing. And if you keep leasing new trucks, the costs stack up fast.

| Factor | Leased to Carrier | Own Authority |

|---|---|---|

| Startup cost | Lower | Higher |

| Control Over Loads | Limited | Full Control |

| Insurance Setup | Covered or Shared | Fully Responsible |

| Fuel Discounts | Often Provided | Must Find Your Own |

| Compliance & Paperwork | Carrier Handles Most | You Handle Everything |

| Gross Pay Rate | Lower (70–85%) | Higher (100%) |

Maintenance and Repairs

Some lease deals include routine maintenance. That can help avoid surprise repair bills. If the truck breaks down, some lease companies even provide a loaner to keep you running.

Buying puts all the repair risk on you. If something breaks, it’s your responsibility. That said, buying a reliable truck or getting a good warranty can help. You also get to choose your own shop and handle maintenance your way.

Leasing a new truck means fewer problems in the early years. That can be a big plus when you’re still learning how to run your business.

Flexibility and Control

Leasing gives you more flexibility. You can return the truck after the term ends or upgrade to something newer. That’s helpful if you’re unsure about how long you’ll be in the business or want to stay up to date with truck tech and fuel rules.

Buying is a bigger commitment. If you need to get out of the truck early, it may take time to sell and you could lose money. But owning means full control. No mileage caps. No wear-and-tear fees. You can drive as much as you want and customize it to fit your style.

Be cautious with lease-purchase programs from carriers. Some drivers report paying a lot with little to show at the end. Not all deals are bad, but some contracts have tight rules and high penalties. Stick with trusted leasing companies and read the terms carefully.

So Buying or Leasing a Semi-Truck?

Leasing helps you get started fast with lower upfront costs. It’s often a good choice if you want a newer truck and fixed expenses.

Buying gives you more value over time. Once the truck is yours, you keep all the profit. No payments, and an asset you can use or sell.

Many owner-operators start out leasing or buying a used truck to get rolling. Once they’re steady, they work toward full ownership.

Pick the option that fits your budget, your goals, and how long you plan to stay in the business.

Everyday Expenses You Will Face as an Owner Operator

Once you’re on the road, the costs don’t stop. Every mile brings expenses — and if you want to make money, you need to know what’s going out. As an owner-operator, you pay for everything. No company’s covering your fuel, tires, or repairs.

Let’s go over the main expenses you’ll face each month.

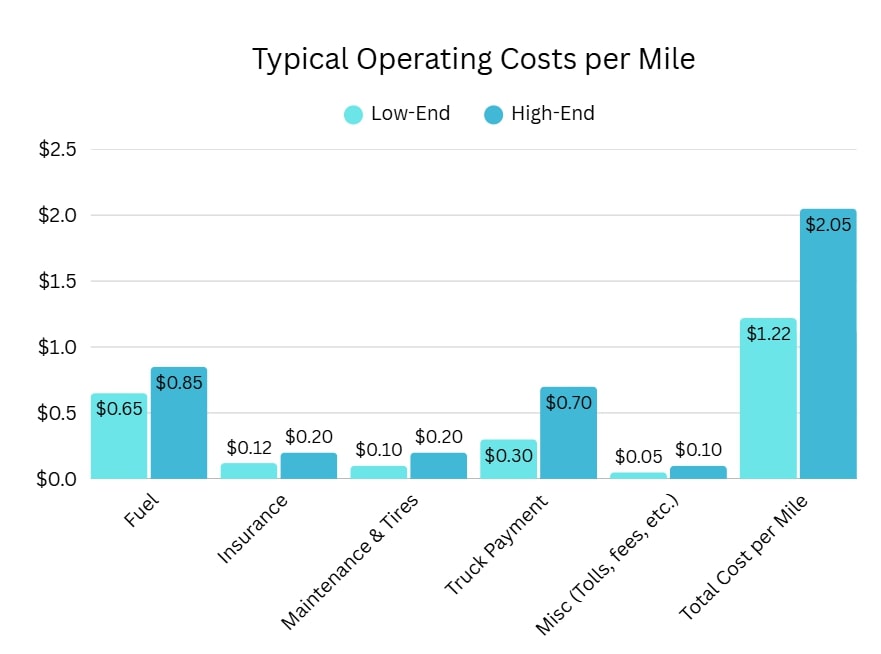

Fuel

Fuel is your biggest bill. No surprise there.

If you drive about 100,000 miles per year, at 6.5 to 7 miles per gallon and fuel around $3.5 per gallon, you’re looking at $50,000 to $54,000 just on diesel.

You can lower that cost. Drive at steady speeds. Cut down on idling. Avoid heavy loads when possible. Use fuel cards or discount programs to get better prices at the pump. And plan your routes to skip deadhead miles.

Fuel prices go up and down. But your fuel bill is always a big deal. Get smart about managing it. Read out guide about 28 practical fuel saving tips to improve your fuel economy.

Truck Payments

If you financed your truck, expect to pay anywhere from $1,000 to $3,000 a month. This depends on how much the truck cost, your loan terms, and your down payment.

If you own your truck outright, that’s one less bill. But even then, it’s smart to save for big repairs or a future replacement. Trucks don’t last forever.

Maintenance and Repairs

Your truck will break. The question is when — not if.

Oil changes, tires, brakes, inspections, filters — these add up fast. Many owner-operators set aside 10 to 15 cents per mile just for maintenance. That works out to about $1,000 per month if you’re running full-time.

It’s also smart to keep an emergency fund for the big stuff. A turbo or transmission can cost thousands. Without a backup plan, one breakdown could put you out of business.

If your truck is leased and includes a maintenance plan, you’ll pay less out of pocket. But most owner-ops cover their own repairs. Keep good records. It helps with resale and shows you’re serious about staying safe and legal.

Insurance

This is one of the most expensive parts of the business — especially in your first year.

You’ll need liability insurance, cargo insurance, and probably physical damage coverage too. If you’re leased to a carrier, they might cover some of this and just charge you a fee. But if you’re running under your own authority, you’ll need your own policies.

For new authorities, it’s common to pay $15,000 to $20,000 a year. Most policies are broken into monthly payments, with a couple months due upfront.

Your rates can improve over time if you keep a clean record. But be ready — hazmat, tankers, or hiring new CDL drivers can drive premiums up.

Permits and Fees

Some costs come once a year. Others show up every few months. You’ll need to budget for:

- IRP plates

- IFTA fuel tax filings

- UCR registration

- Heavy Vehicle Use Tax (usually $550 per truck)

- State-specific taxes (like New York HUT, Oregon mileage tax, or KYU)

- ELD service plans

Each item may be small on its own. But skip one, and you can be fined or shut down. Track everything. Many drivers use a spreadsheet or software to stay organized.

Tolls and Fuel Taxes

If you run the Northeast, Midwest, or Florida, tolls add up fast. Use services like Bestpass or PrePass to manage billing and get small discounts.

Fuel taxes are handled through IFTA. You’ll either owe or get a refund, depending on how much fuel you buy in each state. Just make sure to file your reports on time. Penalties aren’t cheap.

Daily Life on the Road

Even small things cost money:

- Food

- Showers

- Laundry

- Phone and Wi-Fi

- GPS apps

- Load boards like DAT or Truckstop

You can save by bringing your own food or using a fridge and microwave in the truck. If you are up to this, check my guide about easy and healthy meals for truck drivers and see some ideas.

But plan for some daily spending. And don’t forget, if you use a dispatch or factoring service, they’ll take a cut. Dispatchers often charge 5 percent. Factoring companies might take 2 to 5 percent of your load’s value.

Know Your Cost Per Mile

This part is key. Add up all your expenses. Then divide by the number of miles you run. That’s your cost per mile.

Here is what adds up to every mile you spend on the road.

For example, if you spend $8,500 a month and run 10,000 miles, your cost is 85 cents per mile. But if your fuel, insurance, and other bills are higher — say, $17,000 per month on 10,000 miles — your cost per mile is $1.70.

Now imagine taking a load that pays $1.50 per mile. You’re losing money.

You must know your numbers. Aim to run loads that cover your cost per mile and leave room for profit.

Being your own boss sounds good. But it only works if the numbers do. Track every dollar. Cut waste where you can. And always know what you need to earn to stay ahead.

What You Can Really Earn as an Owner Operator?

Owner-operators often earn more per mile than company drivers. But don’t be fooled by the top-line number. Gross revenue isn’t your paycheck, but rather has to cover all your costs.

Let’s break it down: how you get paid, what affects your earnings, and how much you can expect to take home.

How You Make Money?

You get paid either by the mile or by a percentage of the load. If you’re leased to a carrier, you might get 70 to 80 percent of the load revenue. The carrier keeps the rest in exchange for dispatch, insurance, and other support.

If you run under your own authority, you keep the full rate. But now you’re responsible for everything — including load boards, insurance, and compliance. Still, the upside is bigger.

Rates depend on the market. In 2025, dry vans averaged around $2.00 per mile, reefers around $2.25, and flatbeds closer to $2.50. Specialized freight, like hazmat or oversized loads, can pay more.

Company drivers might earn $0.60 to $0.80 per mile as a wage. Owner-operators can gross two to three times that. But remember, you’re also paying for fuel, tires, and every other cost.

Real Net Income

What matters most is what’s left after expenses.

A single-truck owner-operator might gross $150,000 to $250,000 per year. After paying for fuel, maintenance, insurance, and everything else, many net around $50,000 to $85,000.

In a strong year, with few breakdowns and solid freight, you could reach $80,000 or more in profit. In a weak market, or if you get hit with major repairs, you could land closer to $45,000 — or even break even.

According to Indeed, the average owner-operator base salary is $330,000/year. Top performers hit higher numbers by running efficiently, negotiating better, and cutting costs.

| Weekly Gross Revenue | Annual Gross | Estimated Net (After Expenses) |

|---|---|---|

| $4,500 | $234,000 | $70,000–$100,000 |

| $5,500 | $286,000 | $90,000–$120,000 |

| $6,500 | $338,000 | $110,000–$140,000 |

Some teams do gross gross over $350,000, but that often comes with higher expenses too, especially if you run two drivers or haul gear that requires custom equipment.

What Affects Your Pay

Several things make or break your earnings:

- Deadhead miles kill your rate. Plan routes to avoid running empty.

- Poor fuel economy eats into profits fast.

- Downtime from repairs or personal time off means no revenue.

- Freight type matters. Specialized work or direct shipper contracts often pay more.

- The market cycle can raise or drop rates across the board. Some years are good, others are tight.

If the wheels aren’t turning, you’re not earning.

Know Your Minimum Rate

Smart owner-operators set a bottom rate. If it costs you $1.70 per mile to operate and you want to make $0.30 profit per mile, you need at least $2.00 per mile on your loads.

If rates dip below that, you either take a hit or find a better lane.

Load boards can offer high rates one week and low the next. Some drivers prefer to build regular relationships or lease to a stable carrier for consistency.

Owner-operators can gross more than company drivers. That’s the upside. But after expenses, many end up earning $50,000 to $80,000. Not far off a good company job.

The difference is you’re in control. You call the shots. With smart planning and discipline, you can build something solid and you can grow.

But bad decisions or bad luck can eat into your profit fast. That’s exactly what happened to many small carriers and independent drivers during uncertain times and crisis in supply chain. Freight rates dropped after the surge, diesel prices spiked, and volumes shifted unpredictably. A lot of one-truck operations simply couldn’t hold on. They were profitable in boom times, but had no buffer when the market turned.

Stay on top of your numbers. Run efficiently. Cut unnecessary costs. And don’t forget: some of that money has to go to taxes, repairs, and savings. Don’t spend it all just because it hit your account.

Legal and Regulatory Requirements for Owner-Operators

Trucking has rules. Lots of them.

As an owner-operator, you’re not just a driver anymore. You’re responsible for both your driving record and your business paperwork.

This section breaks down the key things you need to stay legal and on the road.

CDL and Endorsements

You can’t drive a truck without a valid Commercial Driver’s License (CDL). If you plan to pull a trailer over 10,000 pounds, you’ll need a Class A CDL.

Getting a CDL usually means:

- Passing a written test to get a permit

- Taking a road test in a truck

- Completing training, often through a driving school (costs range from $3,000 to $7,000)

If you already drive for a company, you likely have this done. But if you’re starting fresh, the CDL is step one.

You can also add endorsements. These allow you to haul special loads:

- Hazmat (H) for anything requiring a warning placard

- Tanker (N) for hauling liquid loads, even in bulk containers

- Doubles/Triples (T) for pulling multiple trailers

Hazmat requires a background check and must be renewed every five years. Endorsements make you more flexible and open the door to better-paying freight.

You also need a valid DOT medical card. That means passing a physical every year or two. As an owner-op, you’re in charge of keeping your own CDL, medical, and compliance files up to date.

You must also follow drug testing rules, even if you’re a one-truck operation. That includes pre-employment and random testing.

Getting Your Operating Authority

If you want to haul freight under your own name and business, you need operating authority. That includes a USDOT Number and an MC Number.

- USDOT Number tracks your safety records and is required in most states

- MC Number gives you permission to haul freight for hire across state lines

You apply online through FMCSA. The fee is about $300. After applying, there’s a 10-day waiting period.

Once approved, you must:

- Buy insurance and have your agent file proof with FMCSA

- File a BOC-3 (this names your legal rep in every state)

- Register for UCR and pay the annual fee

- File your Heavy Vehicle Use Tax (Form 2290)

- Get IRP registration (license plate that works across states)

- Apply for IFTA (fuel tax license)

- Join a drug and alcohol testing program

You’ll also go through a safety audit in your first year. The DOT will check your records to make sure everything is in place.

Leasing to a Carrier

You don’t have to go fully independent. Many new owner-operators lease onto an existing carrier. That means you use their DOT authority. They handle:

- Dispatch

- Insurance

- Safety compliance

- Permits and fuel tax filing

You bring the truck. They bring the paperwork. In return, they take a cut of the load pay, usually around 20 to 30 percent.

This is a good first step for many. You can learn how things work without being buried in forms and fees.

Here are some of the best owner operator companies to consider if you decide to go this direction.

IRP and IFTA

If you run across state lines, two programs matter most: IRP and IFTA.

- IRP (International Registration Plan) lets you use one license plate in multiple states. You pay based on how many miles you run in each state. You’ll pick a base state, apply through its DMV, and get a plate and a cab card.

- IFTA (International Fuel Tax Agreement) helps you report fuel taxes. Instead of tracking tax for each state, you file one quarterly report with your home state. You’ll need to log how many miles you drive and how many gallons of fuel you buy in each state.

If you don’t file IFTA reports on time, your license can be suspended. Many drivers use spreadsheets or software to track this, or let an accountant handle it.

Other Required Permits

A few states have extra taxes or permits:

- KY (KYU number)

- NM (weight-distance tax)

- NY (Highway Use Tax)

- OR (weight-mile tax)

Each one has its own process. If you plan to run in those states, make sure you’re registered before you go.

Compliance and Recordkeeping

Even if you’re the only driver in your business, you must follow the same safety rules as large carriers.

You need:

- A driver file (with medical card, license copies, etc.)

- Maintenance logs

- Hours-of-Service records (usually using an ELD)

- Drug and alcohol testing records

- Proof of insurance

- Copies of all permits and filings

During your first year, FMCSA will audit your business. Keep everything organized and ready.

Getting legal to run your own truck isn’t hard, but it does take time, paperwork, and attention to detail. Once you’re set up, staying compliant becomes routine.

You can hire companies to handle some of this, or start by leasing to a carrier while you learn the ropes. Either way, know what’s required so you don’t get sidelined by paperwork.

Insurance Requirements for Owner-Operators

Insurance is one of the biggest responsibilities you’ll face. You need it to operate legally. You also need it to protect your business from major losses.

Here’s what to know about the types of coverage you may need.

Public Liability Insurance

This is the one required by law. It protects others if you cause an accident. That means damage to property or injury to people.

The legal minimum is $750,000. Most carriers carry $1,000,000 because many brokers and shippers ask for it. If you haul hazardous materials, the minimum jumps much higher. Could go up to $5 million in some cases.

This policy doesn’t cover damage to your own truck. It only covers others if you’re at fault.

Cargo Insurance

This protects the load you’re hauling. If the freight gets damaged, stolen, or lost, this is what pays out.

FMCSA doesn’t always require it. But nearly every broker or shipper will. The typical coverage limit is $100,000. Higher if you’re hauling expensive items.

Plan to buy this along with your liability policy. Without cargo insurance, you’ll have a hard time booking loads.

Physical Damage Insurance

This one covers your own truck and trailer. If you get into a crash, it pays for repairs or replacement. It also protects against fire or theft.

If you took out a loan or lease, your lender will require this. Even if your truck is paid off, it’s smart to keep this coverage unless you have enough cash to replace the truck yourself.

The cost depends on how much your truck is worth. Most policies run between 2 and 5 percent of the truck’s value per year.

You can lower your premium by picking a higher deductible. Some drivers skip this policy to save money, but that’s a risky move unless you have strong savings.

Bobtail or Non-Trucking Liability

This policy covers your truck when you’re not under dispatch. If you’re leased to a carrier, their liability insurance usually only applies while you’re hauling their freight.

Bobtail insurance fills the gap when you’re driving empty or for personal reasons.

If you run under your own authority full time, you won’t need a separate policy like this — your main liability coverage should already include all driving. But lease operators will likely need it.

The cost is low, often just a few hundred dollars per year.

Occupational Accident or Workers’ Comp

Most states don’t require independent drivers to carry workers’ comp on themselves. But some carriers or lease agreements do.

If you don’t have health insurance, this can cover job-related injuries.

Occupational accident insurance isn’t mandatory in every case, but many drivers choose it for peace of mind.

Health and Life Insurance

You’re not part of a company anymore, so you don’t get benefits. That means buying your own health insurance.

If you get hurt and can’t work, you still have bills to pay. Disability insurance and life insurance are smart to look into. They aren’t required, but they matter.

💡How to Shop for Insurance

Start early. Don’t wait until your authority is active. If you apply for operating authority and then can’t get insurance, you’ll waste money and time.

Premiums vary. They depend on:

- Your driving history

- What you haul

- Where your business is based

- How far you run

New authorities usually pay more because they don’t have a safety record yet.

Groups like OOIDA offer access to policies for members. Also, working with an agent who understands trucking can help you avoid costly gaps.

Filing Proof with FMCSA

Once you buy insurance, your agent must file proof with FMCSA. These forms include:

- BMC-91 or BMC-91X for liability

- BMC-34 for cargo

Your authority won’t go active until FMCSA has these on file. The process is usually fast — one or two business days.

Keep digital copies of your insurance certificates. Brokers often ask for them before giving you a load.

Know what your policy includes and what it doesn’t. For example, some plans exclude certain states or won’t cover hazmat unless listed.

Other Legal Items You’ll Need

Besides insurance, here are other important filings and permits.

Unified Carrier Registration (UCR)

Every year, you must register and pay a small fee based on fleet size. For one truck, the fee is about $60 to $70.

You register online. It’s quick. But if you skip it, you could get fined or placed out of service. Mark your calendar and renew every fall.

BOC-3 Filing

This names agents who can accept legal documents on your behalf. You need it to activate your operating authority.

Most drivers use a filing service. Once it’s done, you don’t have to touch it again unless you change your service company.

Heavy Vehicle Use Tax (HVUT)

Every truck over 55,000 pounds must pay this federal tax. It’s $550 per truck per year.

You pay it by filing IRS Form 2290. You’ll need the stamped Schedule 1 as proof — often required when getting plates.

New Entrant Safety Audit

After you start your authority, you’ll be audited sometime in the first year and a half. The DOT will check your paperwork.

They want to see:

- ELD logs

- Maintenance records

- Insurance proof

- Drug testing program info

- Driver file (CDL, medical card, drug test results)

If you don’t have these ready, your authority can be revoked. Keep your records clean from the start.

Hours of Service and ELD

You still have to comply with the Hours of Service (HOS) rules. Usually 11 hours driving, 14 hours on duty, with required breaks.

Most drivers need an ELD. Unless you run short local trips or use a truck built before 2000, you’re expected to log time electronically.

Make sure your ELD is registered with FMCSA and that you know how to use it.

Vehicle Inspections

Do daily checks. You’re required to log any issues.

Also, your truck and trailer must pass a full DOT inspection once a year. Keep the inspection reports with you. Officers will ask to see them.

Drug and Alcohol Rules

Even if you’re self-employed, the DOT still sees you as a commercial driver. You need:

- A pre-employment drug test

- Enrollment in a random testing pool

- An annual Clearinghouse check under your CDL

Keep all test results and documents on file. Missing even one requirement could shut you down.

Hauling Hazardous Materials

If you haul dangerous cargo, there are extra steps. You’ll need special permits, background checks, and a safety plan.

Most new owner-ops avoid these loads early on. But if you go that route, be ready for extra paperwork and oversight.

State-Level Authority

Some states require separate intrastate operating authority. Texas and California are examples.

If you haul loads that never cross state lines, check with that state’s trucking office.

Business Licenses and Taxes

Register your business with your state and the IRS. Get an EIN if needed.

File your taxes. This includes income tax (1099) and, if applicable, payroll tax if you’re paying yourself through a company.

Failing to file taxes won’t just bring IRS trouble. It can impact your business filings or your ability to renew permits.

As you can see, here’s a lot to handle. But once you’re set up, staying compliant gets easier.

Use a spreadsheet, calendar, or compliance software to keep track. Many drivers hire help for drug testing or IFTA reports. It’s often worth it.

Running legal keeps you on the road. Skip something, and you risk getting shut down.

Do it right. Take it one step at a time. Thousands of owner-operators run their business legally every day. You can too.

Business Management for Owner-Operators

Running a trucking business means more than just driving. You also handle freight, money, paperwork, and planning. You’re both the driver and the manager. If either side falls behind, the whole operation suffers.

Below are the business areas you’ll need to stay on top of:

- Finding loads

- Handling your own dispatch

- Setting and negotiating rates

- Tracking income and expenses

- Filing taxes and knowing your deductions

- Making smart business decisions over time

Finding Loads

One of your first questions will be: how do I get freight?

There are five main ways most owner-operators find loads.

Brokers

Freight brokers match shippers with trucks. They talk to the shipper, handle paperwork, and post the job. You get the load. They get a cut — usually around 10 to 20 percent.

The good part is speed. You can get moving fast without hunting down direct customers. The downside is that brokers keep part of the money, so you don’t see the full rate.

Build relationships with brokers who understand your lanes and equipment. Over time, you’ll learn which ones are fair and which ones waste your time.

Load Boards

Load boards are websites or apps where brokers post available freight. You search by location, equipment, weight, and rate. Then you call or message the broker to get the load.

Popular boards include DAT, Truckstop, and 123Loadboard. Full access usually requires a monthly fee.

Load boards are helpful when starting out. You can use them to learn lane rates and find backhauls. But competition can be rough. Many other drivers may call on the same load, which can push rates down.

Check broker credit scores and days-to-pay before accepting a load. Most boards show that info.

Dispatch Services

If you don’t want to call brokers all day, you can hire a dispatcher. Dispatchers search boards, call brokers, and handle booking for you. They charge a fee, often five to ten percent of each load.

You still carry all legal responsibility, but the dispatcher handles the phone work. Be careful who you hire. Some dispatchers are great. Others cause problems.

Also, some brokers won’t work with dispatchers — they want to deal with the carrier directly.

Direct Shippers

Direct freight pays better. There’s no broker taking a cut. But you have to earn it.

You can get direct freight by:

- Reaching out to local businesses

- Asking regular brokers if you can work with the shipper directly

- Cold calling warehouses or manufacturers

- Networking at truck stops or local events

If you land one solid shipper, that can be the difference between chasing cheap loads and building a steady lane.

Load Apps and Digital Tools

Apps like Convoy and Uber Freight let you book loads with a few taps. Many show upfront rates. Some offer fast payment.

Rates vary, but these apps save time. Traditional brokers also offer load apps now, and some let you bid without calling.

It’s smart to keep these tools on hand. Even if you don’t use them often, they can help fill gaps.

Managing Loads and Route Planning

Always think two steps ahead. A big-paying load that drops you in a bad area might not be worth it.

Plan around both legs of the trip. Use load board tools to check load-to-truck ratios in each area. Look for spots where demand is high and rates are better.

Avoid driving empty if you can. Deadhead miles cost you money. Sometimes it’s smarter to take a load that pays less if it brings you into a strong freight zone.

Working with Factoring Companies

If you haul broker loads, you might not get paid for 30 days or more. That can cause cash flow problems, especially with fuel.

Factoring companies pay you quickly, often the next day. They charge a fee — usually around 2 to 5 percent — and collect from the broker later.

They also check broker credit scores, so you know you’ll get paid.

Factoring is optional. If you have money saved or don’t mind waiting, you might skip it. But many owner-operators use it at the start.

At the end of the day, this is your business. You choose how to get loads. You decide who to work with. You plan the routes and negotiate the rates.

Start with tools like load boards. Learn the market. Build connections. Over time, aim for direct shippers and higher-paying lanes.

Know your numbers. Track every cost. Keep your truck moving, but don’t rush into bad deals. With each load, ask: does this move me closer to profit?

Managing Dispatch and Scheduling

When you run a one-truck business, you’re the driver and the dispatcher. That means you’re responsible for where you go, what you haul, and when you haul it. Getting that right can make or break your week.

Here’s how to keep things tight and under control.

Plan Ahead

Try to plan your week in advance. Book an outbound load, then find one coming back — or one that takes you to a good area. Planning a loop or a triangle keeps empty miles low.

Most load boards let you search several days ahead. Things can change fast out there, so give yourself some buffer. Don’t overbook just to fill the calendar.

Use Simple Tools

A calendar app or a notebook can help keep track of pickup times, drop times, and your drive hours. Some owner-operators use Google Calendar. Others go with full TMS software.

Before accepting a load, double-check the timing. Can you finish one delivery and make it to the next pickup legally and on time? If not, pass.

Build a Good Reputation

Brokers and shippers talk. Being on time and staying in touch builds trust.

Let them know if you’re running late. A short call or message goes a long way. That can turn a one-time job into repeat freight.

You’re not just a driver — you’re also the face of your business.

Plan for Rest and Maintenance

Book loads with room for breaks. You’ll need your ten-hour resets and, sometimes, full 34-hour breaks.

Use those resets to handle maintenance. Try to time oil changes or tire checks while you’re off duty. Don’t wait for a breakdown. Plan it.

Handle Admin Time

Once you park for the night, use a bit of time to catch up. Look for your next load. Send signed confirmations. Submit invoices. Update your records.

Many owner-ops do paperwork on a set schedule — like every Wednesday night. Others check load boards daily. Either way, stay consistent.

Know When to Walk Away

Not every load is worth it. Some tie up your truck all weekend for little pay. Others drop in a dead zone with no return loads.

If a load won’t pay enough for your time and fuel, say no. Sometimes waiting brings a better offer. But use your judgment. Every trip costs time and money.

Use Your Tech

Many load board apps can send alerts when loads match your criteria. GPS apps with truck routing help with planning. ELD devices track available hours — check them before booking new loads.

These tools save time and help you avoid mistakes.

Stay Balanced

Overbooking leads to stress, missed appointments, and tired driving. Underbooking can mean lost income. You’ll learn how to balance the load over time.

Keep your truck moving, but keep yourself in shape too. No load is worth a safety violation or a health problem.

Setting Freight Rates and Negotiating

As an owner-operator, you’re in charge of what you get paid. Unlike company drivers, your pay changes with each load. That can work for you — or against you — depending on how you manage it.

Know Your Numbers

You need to know what it costs you to run. That means your cost per mile, or your target daily income.

If your all-in cost is $1.50 per mile and you want $0.50 profit, aim for $2.00 per mile or better.

This number gives you a solid base. It tells you when to accept a load and when to walk away.

Watch the Market

Rates change by lane, region, and season. Use tools like DAT, Truckstop, or market reports to track the average prices.

If a lane usually pays $2.20 and someone offers $1.70, ask for more. It helps if you can show why. Knowing the data gives you an edge.

Talk to Brokers Smart

Be direct, but polite. Ask if the rate has room. Most brokers expect it.

You can say:

- “Fuel costs are up — I’d need a little more.”

- “This goes into a weak market — I’ll need extra to make it worth it.”

- “If you can add $200, I’ll commit right now.”

Avoid bluffing. Don’t mention fake offers. But if you have another real option, it’s fine to bring it up.

Brokers respect drivers who are fair, firm, and clear.

Direct Freight Rates

If you haul for a direct customer, you may set your own flat rate. Consider time, distance, loading effort, and trailer hold time.

For short runs, charge a minimum. For multi-stop or difficult jobs, add fees. Know your value and make sure your price reflects the work.

Don’t Sell Yourself Short

Taking cheap loads too often leads to burnout. It hurts your long-term profit and lowers market expectations.

In down markets, you might run below your target rate just to stay moving. That happens. But don’t make it a habit. Hold the line when you can.

Add Charges When Needed

Extra stops, long wait times, or driver-assist loads should pay more.

Ask for:

- Stop pay

- Detention after two hours

- Layover pay if you’re stuck overnight

Discuss these before taking the job. Make sure they’re written into the confirmation. Keep records in case you need to prove it later.

Fuel Surcharge

In contract freight, a fuel surcharge is often added based on current diesel prices. Spot loads don’t usually list it separately.

But if fuel is high, you can ask for extra money to cover it. Frame it as part of your rate, even if it’s not a line item.

Justify Higher Rates

Short hauls, tight deadlines, tough areas like New York City — all should pay more.

So should heavy loads, hazmat, or oversized freight. If the job asks more of you, don’t be afraid to quote higher.

You won’t win every load. But over time, if you deliver good service, some brokers will pay more just to keep working with you.

Payment Terms

Getting paid matters too. Most brokers pay in 30 days. Some offer quick pay in 1 to 2 days for a fee.

Check broker payment records. Some are slow to pay. You can negotiate the quick pay fee or use a factoring company if needed.

If you have the cash to wait, you can skip factoring. But early on, many owner-operators use it to keep fuel money in hand.

Dispatch and rate-setting go hand in hand. Book smart loads. Know your numbers. Talk clearly. Be fair, but don’t be afraid to push when the job calls for more.

Every extra $50 per load adds up over a year. And every hour you save with better planning keeps you in the game longer.

This is your business. Treat it like one. Learn from every call. Improve with every trip.

Accounting and Bookkeeping for Owner-Operators

Managing money is a big part of running your own trucking business. Without solid records, it’s easy to lose track of what’s coming in and going out — and that’s how some drivers find themselves broke without knowing why.

Good bookkeeping doesn’t just help at tax time. It gives you a clear picture of whether your business is making money or just spinning its wheels.

Keep Business and Personal Money Separate

Start by opening a bank account just for your trucking business. Put all income into that account and pay your business expenses from it.

Even if you’re a sole proprietor, this makes everything cleaner. If you set up an LLC or corporation, it’s a must. Mixing funds can cause problems with taxes and may hurt your legal protection.

Consider a business credit card or fuel card too. These help you track expenses automatically and come with detailed statements.

Track Every Dollar

You need to record what you earn and what you spend — every single time.

Use a spreadsheet, QuickBooks, or a trucking-focused tool like RigBooks or TruckingOffice. Log every load’s pay. Keep every receipt.

Your expenses will fall into categories like fuel, insurance, truck payments, maintenance, tolls, meals, phone, and more. Update this weekly so you don’t get buried in paperwork later.

Some apps let you connect to your bank and auto-import transactions. That can save time and reduce mistakes.

Know Your Cost Per Mile

Track how much it costs to run your truck for every mile you drive.

You can break it down into fuel cost per mile, maintenance cost per mile, insurance per mile, and so on. This lets you see where your money is going.

If fuel costs suddenly jump, it could be time to ease off the pedal. If repairs are climbing, maybe it’s time to look at a newer truck or shop around for parts.

This kind of analysis is only possible with clean records.

Pay Yourself the Right Way

If you’re a sole proprietor or a one-person LLC, you probably take a draw from the profits — money for yourself after expenses. If you’ve set up an S-Corp, you may pay yourself through payroll.

Whatever your setup, record everything. Don’t pay personal bills straight from the business account unless you log it properly.

A good accountant can help you decide the best setup. Going the S-Corp route might save on taxes, but it brings more paperwork. It’s only worth it if you’re making enough profit.

Save All Documents

Keep every receipt — or take photos and store them digitally. There are apps for this.

Save your bills of lading, rate confirmations, and maintenance receipts too. These are needed for taxes and sometimes for safety compliance.

Hold onto these for several years just to be safe. The IRS and DOT both have document rules, and you don’t want to be caught without the right paperwork.

Consider Hiring a Pro

You don’t need to do everything alone.

Some owner-operators hire accountants or use companies that specialize in trucking. These pros can handle monthly records, send you reports, and file your taxes.

They also know the ins and outs of trucking deductions — what you can write off, when to buy equipment, and how much to set aside for taxes.

Their fee is also a business expense. And if they save you from one big mistake, they’ve more than paid for themselves.

Build a Budget and Manage Cash Flow

Trucking income can be feast or famine. One week you get a big check. The next, nothing.

Plan for this. Budget ahead for your fixed bills like insurance and truck payments. Keep something in reserve for emergencies or gaps in work.

A good target is a few months of expenses saved up. If that’s not possible yet, start small. Even a basic cushion helps.

Watch Your Profit and Loss

Every month or quarter, create a report showing what you earned and what you spent. This is called a profit and loss (P&L) statement.

Let’s say you grossed $40,000 in a quarter and spent $30,000 to run. That leaves $10,000 profit. Not bad — but where did the money go?

Maybe $18,000 went to fuel. That’s nearly half your gross. Can you cut that? Slower driving or a better route might help.

Or maybe repairs ate into your profits. Time to look at trade-in options. But you won’t know unless the numbers are there.

Track Your Invoices

If you’re working with more than one broker or shipper, you must stay on top of billing.

Send out invoices right after delivery. Keep a list of who owes you and when they’re supposed to pay. If someone goes past the agreed time, follow up.

If you use factoring, they’ll handle some of this — but they’ll also take a cut. If not, you’re your own billing department.

Some apps like QuickBooks let you send professional invoices and track payments automatically.

You don’t have to love bookkeeping, but you do have to do it. Many great drivers have failed because they didn’t manage their money right.

A few hours each week keeping things in order can save your business down the road. Clean records help you make smart choices, stay compliant, and keep more of what you earn.

Treat it seriously. Because at the end of the day, the numbers don’t lie.

Tax Considerations for Owner-Operators

When you run your own truck, taxes are a whole different game than when you’re on a company paycheck. You’re not just a driver — you’re running a business. That means you take on more responsibility, but you also get access to bigger deductions and more ways to keep your income.

Understanding Self-Employment Taxes

If you’re a sole proprietor or operating as a single-member LLC, you’ll need to pay self-employment tax. This covers Social Security and Medicare and currently adds up to about 15.3 percent of your profit.

That’s more than what company drivers pay because you’re covering both the employee and employer portions. The bright side? You can deduct half of that when figuring out your income taxes.

Some drivers switch to an S-Corp once profits are high enough — usually over $70,000 to $100,000 net — because you can split income between payroll and business profit, which may reduce your tax hit. But it adds paperwork. A good accountant can help you decide when or if that switch makes sense.

Quarterly Tax Payments

Unlike a regular paycheck where taxes are taken out automatically, I’ve had to make quarterly estimated payments. It’s something you don’t want to ignore — the IRS expects payments four times a year (April, June, September, and January).

You’ll be covering both income tax and self-employment tax. A general rule: if you expect to owe over a thousand bucks in taxes for the year, you should be paying quarterly.

Many folks play it safe by sending in what they owed the previous year, divided by four. Another approach is to stash away around 25 to 30 percent of every load into a savings account. When tax time comes around, you’ll have the cash ready.

What You Can Deduct

The tax code gives you a big toolbox to legally reduce your tax bill. Pretty much anything that’s a normal business expense is fair game.

Common deductions include:

- Fuel, tires, repairs, oil changes — all your on-the-road operating costs

- Loan interest on your truck or trailer (not the principal)

- Truck depreciation — often using Section 179 or bonus depreciation in year one

- Insurance — including liability, cargo, and health coverage for yourself

- Fees like IFTA, IRP, UCR, and other permits

- Per diem — instead of tracking every food receipt, you can deduct a flat amount per day away from home (80 percent of $69 per day, increasing to $80 late in 2024)

- Lodging, if you ever stay in a motel during breakdowns

- Cell phone, internet — the business portion

- Office supplies and postage

- Accounting or legal fees

- Interest from business credit cards or financing

- Memberships or subscriptions — OOIDA, load boards, etc.

- Parking fees, truck washes, tolls

- Tools, gloves, boots, safety gear, GPS, CB radio — if used for the business

Even small stuff counts. I’ve deducted everything from flashlights to gloves — those minor costs add up over the year and help reduce what I owe.

Payroll or Owner Draw?

If you’re not an S-Corp, you’ll just draw money from the business account and report it as profit. That’s normal for sole props and single-member LLCs.

If you go the S-Corp route, you’ll need to put yourself on payroll, with regular paychecks and filings. That setup might save on taxes, but it comes with extra paperwork and only pays off once you’re making consistent profit.

Keep Records

Receipts, logs, invoices. Save them all.

Use a scanner app or snap photos of your receipts and store them digitally. Keep your tax returns and records for at least three years. If you claim per diem, your daily logs are usually enough to prove travel days.

Also, don’t forget to deduct your Heavy Vehicle Use Tax. That $550 annual fee is a business expense.

Don’t Forget State Taxes

If your state collects income tax, you’ll need to file and possibly pay estimates there too. Some states also charge business-specific fees — like Texas with its franchise tax — so check the rules where you’re based.

Tax Credits and Other Breaks

There aren’t many tax credits specific to trucking, but some general credits still apply. If you qualify for things like the Child Tax Credit or Earned Income Credit, use them.

Occasionally, there are also credits for eco-friendly trucks or hiring certain workers, but most single-truck operations won’t deal with those.

Use a Pro When You Can

Tax laws change, and there’s money on the table if you don’t know what you’re doing. Working with a tax pro — especially one who understands trucking — can help you stay legal while saving every dollar you can.

They can help you decide when to buy equipment, when to switch structures, and how to report everything correctly. Even if you do most of the work yourself, a year-end review is a smart move.

About Per Diem Programs

If you’re running under your own authority, you can claim per diem directly on your tax return. If you’re leased onto a carrier, they might offer a per diem pay plan where part of your settlement is tax-free — but they usually charge a fee for it.

Compare the benefit of doing it yourself versus letting the carrier handle it. Many independent drivers come out ahead by claiming the deduction on their own.

Taxes are a part of the game, and the better you understand them, the more you’ll keep in your pocket. Good recordkeeping, smart deductions, and planning ahead are what separate a stressed-out driver from one who’s in control.

Paying taxes is part of the deal. But with the right habits, you can keep more of your money and build a stronger business in the long run.

Final Thoughts on Becoming an Owner-Operator

Owning and running your own truck isn’t just another driving job. It’s a full-on business. You wear two hats every day — the driver and the owner. That’s a big responsibility, but also a big opportunity if you approach it the right way.

Here’s a quick summary of what matters most:

Start with a Solid Plan and Enough Cash

Before you hit the road, know what you’re getting into. Buying or leasing a truck, insurance, permits, and early repairs all take money. One of the biggest reasons new owner-ops fail is they run out of cash too soon. Make sure your financial base is steady before taking the leap.

Handle the Paperwork Right from the Start

It’s not just about having a CDL. You’ll need to get DOT and MC numbers, IFTA registration, IRP plates, UCR, HVUT, and the right insurance. Missing even one of these can get you fined or sidelined. I built a compliance checklist early on, and I keep it updated — it saved me more than once.

Watch Every Dollar

This business runs on thin margins. Track every expense and know your cost per mile. Use that number when deciding what loads to haul. If fuel takes up a third of your income, then driving smart and comparing fuel card deals makes a real difference.

Choose Your Hauls with Care

Long-haul, regional, or specialized — each has its ups and downs. Make sure the freight you haul fits your goals and your lifestyle. If you’re running long miles, they better be paying. And always think about your next move — don’t get stuck deadheading into weak markets.

Build Freight Relationships

In the beginning, you’ll probably rely on load boards and brokers. But over time, try to build connections — with trusted brokers or even better, direct shippers. These relationships can smooth out your schedule and make your income more predictable.

Get the Right Protection

Don’t cut corners on insurance. Cargo, liability, physical damage — it all matters. And so does safety. Keep your CDL clean, follow HOS rules, and maintain your truck. One major accident or DOT violation can shut your whole business down.

Stay on Top of the Business Side

Bookkeeping, taxes, permits — it’s not glamorous, but it’s what keeps you in business. Use software or apps to make it easier, but always know where your money’s going. Take advantage of tax deductions like per diem and depreciation, and file on time. If it gets overwhelming, hire someone who knows trucking.

Be Ready for Setbacks

Breakdowns, rate slumps, illness — they happen. Have some emergency cash set aside. Even a few thousand dollars can keep you moving when something goes wrong. A line of credit or a maintenance fund can be a lifesaver when the unexpected hits.

Keep Learning

This industry changes all the time. New rules, new rates, new tech. Keep up with the news, talk to other drivers, and don’t be afraid to adjust how you operate. The drivers who keep learning are the ones who stay in business the longest. I’ve learned more from other owner-ops in forums and parking lots than from any manual.

You’re in Control

This career path isn’t for everyone, but if you’ve got the drive and a clear plan, it can be one of the most rewarding ways to work in trucking. You control your time. You choose your loads. You build your own success — mile by mile.

It’s tough, especially in the beginning. But if you run smart, stay organized, and take care of both the driving and business ends, you’ll be way ahead of the pack. Hopefully, this guide gave you the clarity you need to move forward.

Take the time to prepare. Ask questions. Talk to drivers who’ve done it. And when you’re ready, give it your all.

Safe travels, and good luck out there.